A Year Since CECL: Capital Expected to Be Most Impacted

In the 13 months since the Financial Accounting Standards Board (FASB) finalized its new standard on accounting for credit losses, ASU 326, financial institutions have been preparing to implement what has been labeled by some industry figures as the biggest change ever to bank accounting.

Although institutions will not be required to implement the current expected credit loss model, or CECL, before Dec. 15, 2018, at the earliest, bankers and their advisors have been researching requirements of the updated standard, determining what data will likely be needed and exploring possible methodologies for their calculations of the allowance for loan and lease losses (ALLL). This has required them to consider how their institutions will be affected by the change – both from an organizational standpoint and a financial standpoint.

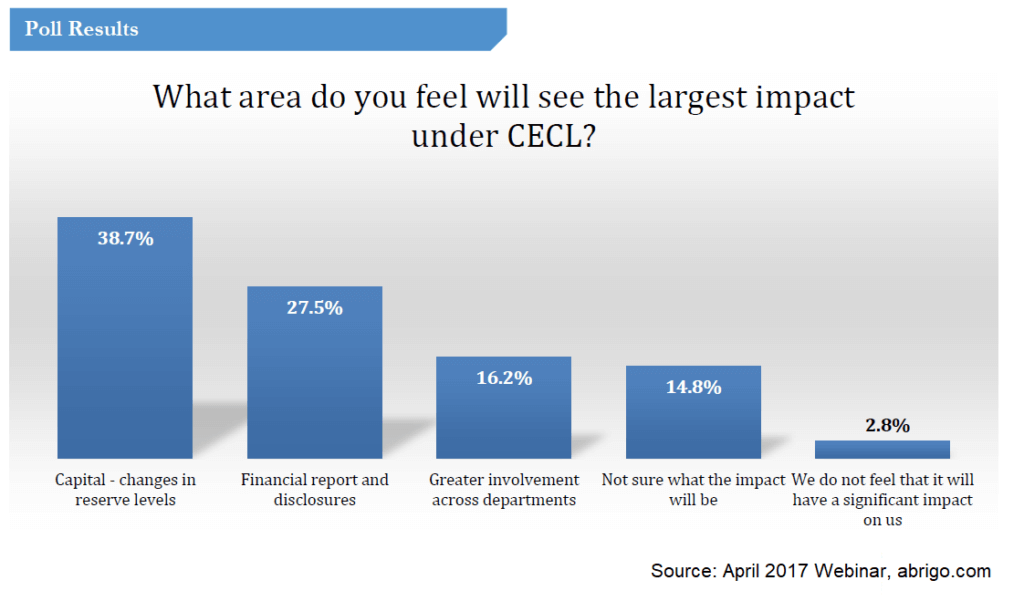

Based on our surveys, financial institutions expect the largest impact under CECL will be related to capital and changes in reserve levels. During a session of the CECL Methodology Webinar Series in April, we asked more than 200 community financial institution managers and executives, “What area do you feel will see the largest impact under CECL?” Capital was selected as the answer by 39 percent of respondents.

Regulatory agencies have said that the earlier recognition of credit losses under CECL will likely increase allowance levels and lower the retained earnings component of equity upon initial adoption. However, agencies have noted that the actual effect of CECL at implementation will vary by institution and depend on factors such as the institution’s portfolio mix, underwriting practices, etc. Regulators plan to monitor changes to institutions’ regulatory capital as the new credit loss methodology is adopted.

Learn more about navigating the CECL transition.

Disclosures for CECL

After capital, financial institution executives surveyed by Abrigo most often cited financial reporting and disclosures as being the areas most impacted by CECL, with 28 percent of respondents selecting this choice.

Disclosures under the new accounting standard should allow financial statement users to understand:

• The credit risk inherent in the portfolio and how management monitors it

• Management’s estimate of expected credit losses, and

• Changes to the estimate of expected credit losses that have taken place during the period.

Cross-functional teams for CECL

For 16 percent of survey respondents, the area most impacted by CECL is expected to be the greater involvement across departments in the ALLL calculation. Experts have said developing cross-functional teams (with credit knowledge and accounting knowledge) for CECL implementation may help ensure that assumptions and inputs used to develop the allowance are the most accurate and aren’t in conflict with those used for conducting stress tests.

Abrigo’s survey also found that uncertainty continues to be a factor for some financial institutions as it relates to CECL implementation. Approximately 1 in 7 respondents said they are not sure what the largest impact of CECL will be. Only about 3 percent of respondents said they don’t expect CECL to have a significant impact.

Regardless of which area of the institution will be impacted most, it is clear that CECL implementation planning is underway, and it poses a range of challenges to the current processes of estimating credit losses at banks and credit unions. In other surveys by Abrigo, financial institution executives have indicated that introducing new financial models, executing various methodologies and data retrieval are their biggest challenges of CECL implementation planning.

To learn more about CECL, visit the CECL software overview or ALLL.com, a comprehensive resource for the allowance for loan and lease losses.

Additional Resources