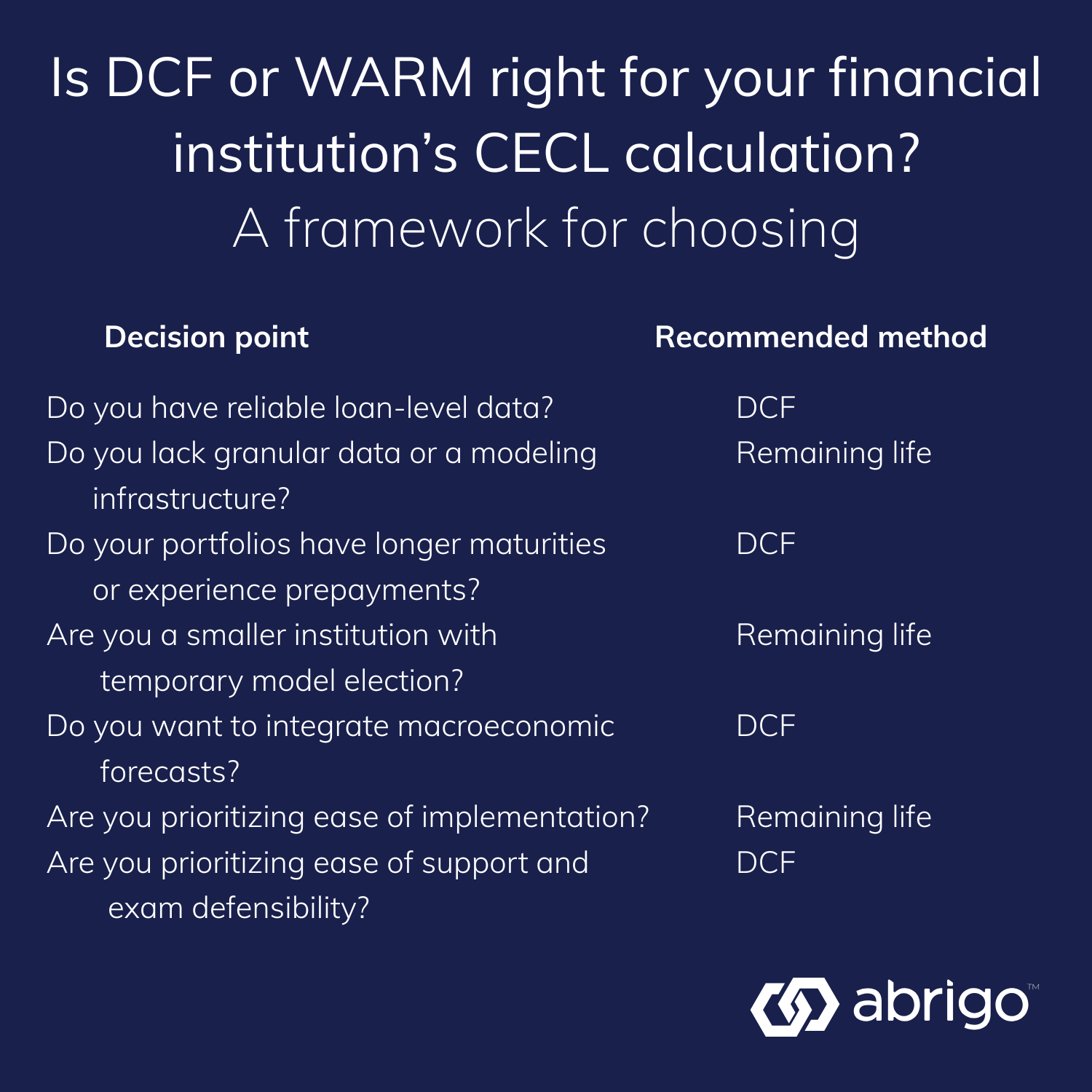

What is the discounted cash flow method?

The DCF method estimates credit losses by projecting future contractual cash flows, applying assumptions for prepayments, defaults, and recoveries, and discounting those expected loan-level cash flows back to present value using the effective interest rate (EIR) as defined by the FASB.

As ASC 326-20-30-4 says, “The allowance for credit losses shall reflect the difference between the amortized cost basis and the present value of expected cash flows.”

How it works

The discounted cash flow methodology, in essence, uses contractual schedules adjusted for prepayments to estimate future balances by month. This is extraordinarily helpful when adhering to ASC 326-20-30-6, which instructs institutions to model “expected credit losses over the contractual term of the financial asset(s).”

ASC 326-20-30-6 also says “ An entity shall consider prepayments as a separate input in the method or prepayments may be embedded in the credit loss information.” Speaking from experience, it’s neither an easy nor fun task to defend changing expected lives due to changes in prepayment speeds in varying rate environments when prepayments are “embedded in the credit loss.”

This approach, whether discounted or undiscounted, offers the opportunity to eliminate a life assumption, which is the most difficult and material assumption to support in a remaining life model (described below).

In fact, in order to support the remaining life input, one must run cash flows adjusted for prepayments, which begs the question – why not just stop there? As an added opportunity, forward-looking amortization schedules, interest income, and periodic expected loss all provide a strong foundation from which to manage. After all, it is the language of banking.

Armed with this kind of output, estimating future balances is accurate, which can allow for production budgeting. Loan-level detail on interest income that considers the default probability is also helpful in its own right. Lastly, timing-specific loss estimates make backtesting, monitoring, and scenario analysis feasible.