Yet across much of the industry, staffing levels remain flat. Many credit and lending leaders at equipment finance firms may soon face a widening gap between market opportunity and operational bandwidth.

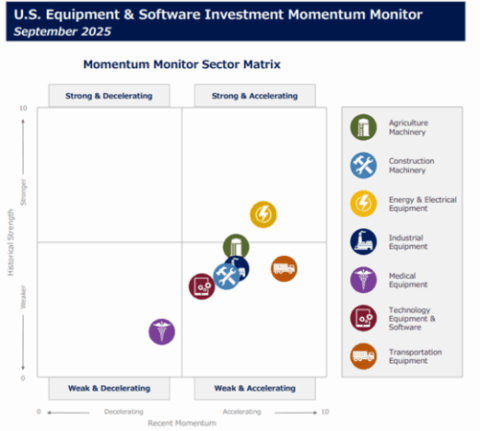

Source: U.S. Equipment & Software Investment Momentum Monitor, Sept. 2025, ELFA

This familiar challenge of growing volume without growing overhead will require more than simply capital to fund new deals. It demands a shift toward efficient equipment finance: operationally lean, technologically enabled, and built to scale. Workflow automation helps firms scale with demand while protecting profitability.

Efficient financing operations matter to growth

Equipment finance, where both leases and loans are products, isn’t like traditional lending. The operational complexity, which includes residual value analysis, multi-party vendor programs, property and sales tax compliance, and asset-level tracking, adds complexity at every stage of the contract lifecycle from origination to asset disposition.

Firms with manual or siloed processes can face delays, compliance risks, and missed opportunities.

Meanwhile, borrower and equipment vendor expectations are evolving. They want faster decisions, seamless documentation, and real-time updates. Equipment financing companies that can’t deliver on these needs risk losing repeat business or falling behind more agile competitors, including fintechs and alternative lenders.

Efficient equipment finance firms can more easily scale, serve clients faster, and respond to market shifts without overextending their teams.