FASB Proposed CECL Extension: The True Impact

CECL implementation timelines have been altered since the release of this post. Find updated information here.

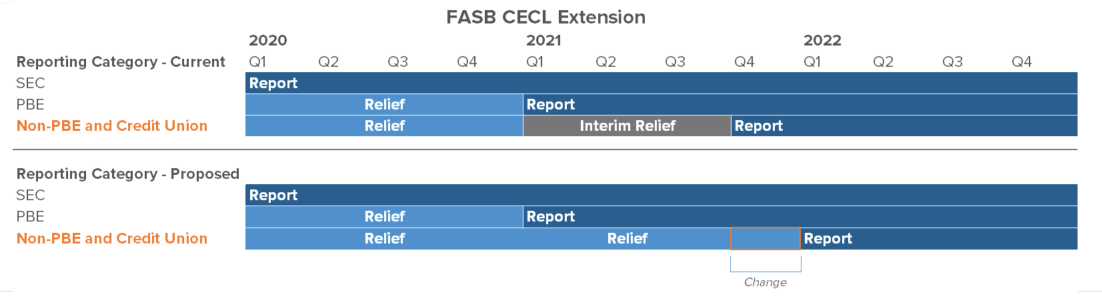

The Financial Accounting Standards Board (FASB) recently introduced a proposal to allow calendar year-end non-public business entities (PBEs) to report reserve levels in accordance with the new current expected credit loss (CECL) standard on Mar. 31, 2022, instead of the initial reporting date of Dec. 31, 2021. This was initially discussed in a regulatory meeting in June and the relief period was further solidified in a board meeting last week.

FASB issued the final CECL standard on June 16, 2016. After the financial crisis in 2007-2008, the FASB decided to revisit how banks estimate losses in the allowance for loan and lease losses (ALLL) calculation. Currently, the impairment model is based on incurred losses. The model will be replaced by CECL, where losses need to be projected over the life of the loan.

Although the new proposal may look like FASB is delaying the CECL implementation timeline by a year, with this change non-PBEs essentially have 90 more days to report reserve levels in accordance with the standard.

“We all know how fast 90 days can fly by. I am concerned by some of the headlines regarding this proposal as they imply that institutions have an additional year when in reality they have an additional quarter,” said Neekis Hammond, Managing Director at Abrigo. “Many will read no further than the headline and alter their transition plans. The worst thing that can happen to any institution is to plan for an additional year erroneously.”

Learn more about navigating the CECL transition.

Without this proposed change, these institutions would have to adopt CECL on their call reports for the “annual period” of 2021 to meet the Q4 reporting date. To accomplish this, interim statements would have to be produced throughout the initial fiscal year, causing two calculations to be made: one at the end of Q4 2021 and one in Q1 2022. This would result in a large provision expense for a year sitting in one quarter.

With the proposed change, this will no longer be the case. The catalyst of the proposal was to eliminate the awkwardness of the interim statements, not to provide more time. Removing the previous year’s interim statements is not delaying the implementation timeline, only improving its reporting requirements.

What to do with the change

In the suggested relief period of 2021, institutions should be calibrating their models to what the market is doing and running CECL calculations in parallel to incurred loss calculations. This full (instead of partial) relief period will not work as intended if institutions are not calculating CECL throughout the year and observing results.

Shayne Kuhaneck, an assistant director at FASB, stated during a CECL implementation webcast this week for community banks, “I travel around to quite a few different venues, speaking to a pretty broad swath of stakeholders. The consistent message is that data continues to be challenging, and so I would recommend not slowing down and I would recommend continuing to collect that data and if you haven’t started, to start, to see where your gap is. While you have the extra time, I think it’s a perfect opportunity to keep moving forward with your plans.”

Hammond supported Kuhaneck’s comment and added, “True relief is being in a position to leverage the resources of larger and potentially more sophisticated organizations. This is best performed by observing reported allowance levels of SEC registrants and Public Business Entities. As these entities report quarterly and annual financial performance, non-PBEs will be able to calibrate their models as appropriate. I’m not implying that non-PBEs should “back into” their reserve level, rather, as non-PBEs look to utilize less sophisticated models calibrating them to more sophisticated models is a necessary step in the transition process.”

A draft of the proposed update is currently being worked on, with an upcoming vote by written ballot. The proposal will have a 30-day comment period before being confirmed.

Whitepaper: Top 10 CECL Tips

Webinar: Best Practices for Running and Validating a CECL Model