Interest Rate Risk is the potential for loss of future income or economic value of equity caused by an adverse change in interest rates. If we go one step further, economic value analysis estimates the sensitivity or change in the economic value of equity to changes in interest rates. Depending on your charter this is Economic Value of Equity (EVE), Net Portfolio Value (NPV) or Net Economic Value (NEV) sensitivity. Economic value analysis uses the full cash flows of a financial institution’s assets and liabilities, so it summarizes information about expected earnings over a much longer time period than a 12 to 36 month income forecast. Thus, it is a measure of your long-term earnings capacity.

Because the future is uncertain, no one can consistently predict the future course of interest rates. The correct message from this analysis is that you should position your risk exposures so you can live with a wide range of interest rate changes. Modeling starts with net present value (NPV), which is the current value of all cash flows received in the future; calculated by discounting the cash flows at an appropriate interest rate, which is referred to as the discount rate.

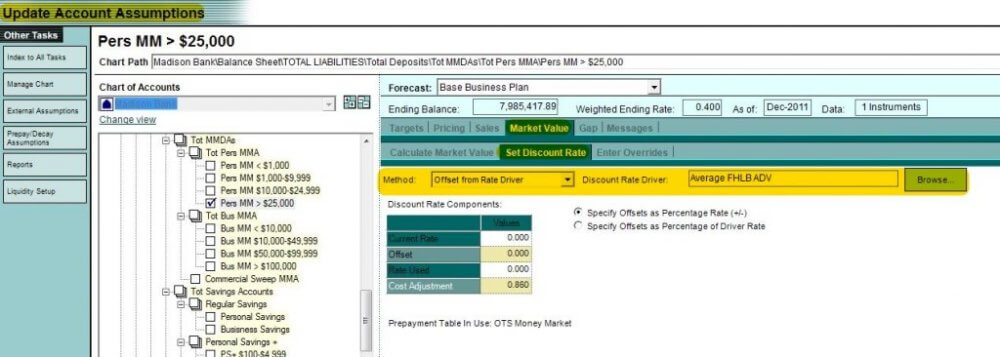

The process of measuring IRR with economic value analysis is relatively straightforward. First determine the economic value of most assets and liabilities, at current market rates, which involves discounting the cash flows to estimate a net present value. The net present value of the assets and liabilities are then used to calculate the economic value of equity. Finally the same process is calculated again with increased or decreased market rates. Interest rate risk is measured by the change in the economic value of equity from the current rate to each of the increased or decreased market rates.

Running a current market value report is like the end of period balance sheet. The economic value analysis measures the risk from assets and liabilities currently on the balance sheet. Economic value of equity is a measure of a financial institution’s earning capacity and the analysis tries to determine how its earning capacity is affected by changes in interest rates. What this means is a current market value report is a static report and does not take into account any future new money or alternative forecast strategies.