Survey: Most Banks are Collecting, Analyzing CECL Data

Community bankers in the throes of implementing the current expected credit loss model, or CECL, are generally collecting and analyzing data at this point in the process, according to a new survey on banks’ CECL status.

Learn more about navigating the CECL transition.

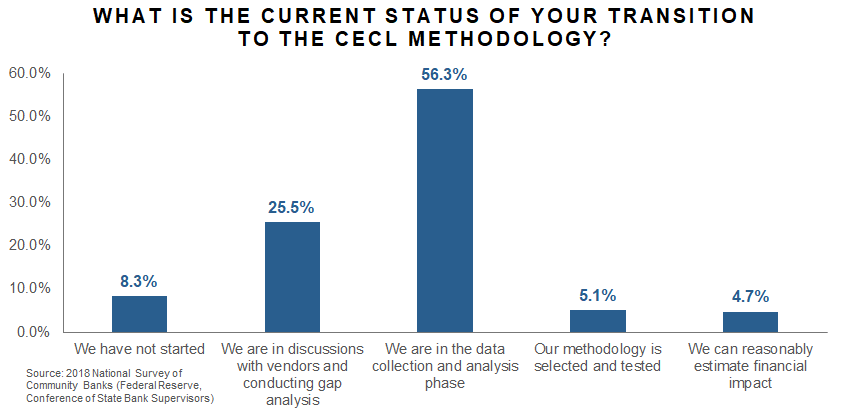

In the 2018 National Survey of Community Banks, bankers were asked about the current status of their transition to the CECL methodology. Among 521 respondents, 56.3 percent said they are in the data collection and analysis phase. A quarter (25.5 percent) are in discussions with vendors and conducting gap analyses and 5.1 percent have selected and tested their methodologies for the accounting standard update. Interestingly, 4.7 percent of respondents said their institutions can reasonably estimate the financial impact of adopting CECL.

At the other end of the preparedness spectrum, 8.3 percent of those surveyed said they haven’t started the transition to CECL. Banks that file with the Securities and Exchange Commission (SEC) must comply with CECL in 2020; all other financial institutions have until the following year.

The survey was released by the Federal Reserve, the Conference of State Bank Supervisors and the FDIC as part of the Sixth Annual Community Banking Research and Policy Conference, and it was conducted by state bank commissioners. Additional detail on CECL efforts wasn’t provided in the survey results, except for a few comments from bankers.

The survey was released by the Federal Reserve, the Conference of State Bank Supervisors and the FDIC as part of the Sixth Annual Community Banking Research and Policy Conference, and it was conducted by state bank commissioners. Additional detail on CECL efforts wasn’t provided in the survey results, except for a few comments from bankers.

“Community bankers expressed concern that CECL, which is intended to address delays in the recognition of loan losses, will complicate collection of data on loan quality,” the report said. It quoted one surveyed banker as saying the following:

“Implementation of CECL is overly complex and far-overreaching for an institution as noncomplex as ours. The burden and the cost of CECL may have an impact on an institution’s willingness to lend in the future. It is virtually impossible to administer absent highly advanced and expensive experts or systems.”

For financial institution staff with questions about implementing CECL, Abrigo hosted a panel discussion that addressed questions about the transition, organizational changes and other issues. An on-demand replay is available here. In addition, community banks looking for realistic and approachable steps for complying with the CECL changes can learn more in the whitepaper, “A Practical CECL Action Plan.”

Additional Resources

Webinar: Data Quality: Methods for collecting adequate data in preparation for CECL

Whitepaper: CECL Solution Buyer’s Guide