Banks and credit unions inherently want to originate only the best loans, but that isn’t a reality in the banking world today. In an increasingly competitive environment, institutions look for earnings and efficiency gains. Many institutions look for these gains through expense cuts, but loan pathing may be a solution.

Loan pathing is the process of mapping the path that various loan applications follow, based on the application’s characteristics. The goal is to improve or optimize how loans are handled, and typically institutions implement this for only small to mid-sized loans. Loan pathing incorporates software and workflow management to ensure fast decisioning and a lower average origination cost.

It is a relatively new concept that has been brought to life with the advancement in lending software and automation. In recent years there has been an obvious shift in customer expectations due to the availability of technology. No matter the industry, customers expect speed and accuracy. A slow loan decisioning process directly affects the customer experience and makes it difficult to win loans against competitors that can respond more quickly.

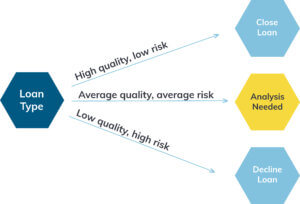

When a loan application is received by an institution, in some instances it can be immediately weeded out or approved. But without a system in place to flag these obvious applications, all loans follow the same, laborious path, and analysts spend too much time on the strong and weak loans.

If an application is strong – based on the criteria and thresholds set by the institution’s credit policy –give it a quick approval to prevent competition from approving it first. Losing a deal on a strong loan leads to missed interest income and cross-sale opportunities down the road.

Likewise, if a weak and risky loan enters the pipeline, it should also warrant a quick response. Every extra minute spent on evaluating a loan that inevitably will be denied is a waste of time and resources. By speeding up the application process for those loans, more time can be spent on evaluating the loans in the middle range. Former bank president Neill LeCorgne said in a recent whitepaper on loan pathing, “...applications in the middle should receive the most attention from commercial lenders, credit analysts, and approving officers, because making decisions for these loans is an art.” The loans in the middle are the ones that have the largest impact on returns and risk if not handled correctly.

In an upcoming webinar, Loan Pathing: Fast Track Your Decisioning, Neill LeCorgne will discuss how to set up an effective loan pathing process at your institution. If used effectively this combination of automation and workflow management will help an institution improve the borrowing experience while also focusing resources on the loans that need more analysis.