The Main Street Lending Program has opened for lender registration. To learn more about MSLP updates, click here. To receive updated information on any new round of PPP funding and how lenders can participate, subscribe to our newsletter.While community financial institutions have been focused on the Small Business Administration’s Paycheck Protection Program (PPP), the Federal Reserve recently unveiled a new loan-purchase program, the Main Street Lending Program (MSLP). Under the Main Street Lending Program, the Fed has pledged $600 billion to help middle-market businesses weather the economic shock caused by the coronavirus pandemic. The MSLP establishes three loan facilities, the Main Street New Loan Facility (MSNLF), the Main Street Expanded Loan Facility (MSELF), and the Main Street Priority Loan Facility (MSPLF). Like the PPP, the MSLP seeks to support the economy by providing economic relief to local businesses across the country. An average of two-thirds of every dollar spent at local businesses stays in the community, according to the Small Business Economic Impact Study by American Express. Also, as with the Paycheck Protection Program, community financial institutions will play a vital role in the Main Street Lending Program. Eligible lenders for the MSLP include U.S. insured depository institutions, U.S. bank holding companies, and U.S. savings and loan holding companies. However, whereas the PPP applied solely to small enterprises, the MSLP expands aid to mid-sized businesses. The Fed program allows eligible lenders to originate new loans or increase the size of existing loans to businesses with up to 15,000 employees or $5 billion in 2019 annual revenues. There is no minimum number of employees, so smaller borrowers can take advantage of both the MSLP and the PPP. However, the minimum loan size for the MSNLF and MSPLF is $500,000 and $10 million for MSELF loans.

Main Street Lending Program Offers Loan-Purchase Option to Lenders Helping Businesses

April 15, 2020

0 min read

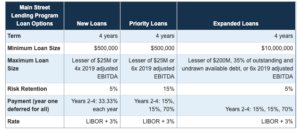

The four-year loans would have one-year deferred payments of principal and interest, and be offered at adjustable rates of LIBOR (1 or 3 months) plus 300 basis points.

Main Street Expanded Loan Facility (MSELF) Terms

For expanded loans to current customers, the maximum size loan available under the MSELF would be the lesser of (i) $200 million, (ii) 35% of the borrower’s outstanding bank debt, or (iii) an amount that, when added to the borrower’s existing debt, does not exceed six times the borrower’s 2019 EBITDA. MSELF loans have a principal amortization of 15% at the end of the second year, 15% at the end of the third year, and a balloon payment of 70% at maturity at the end of the fourth year, according to the term sheet.

Main Street New Loan Facility (MSNLF) Terms

New unsecured loans, according to the term sheet for the facility, could be made up to the lesser of (i) $25 million or (ii) an amount that, when added to the borrower’s existing debt, does not exceed four times the borrower’s 2019 EBITDA. MSNLF loans have a principal amortization of 33.33% the second, third, and fourth year.

Main Street Priority Loan Facility (MSPLF) Terms

The maximum loan size for MSPLF loans is the lesser of (i) $25 million or (ii) an amount that, when added to the borrower's existing debt, does not exceed six times the borrower's 2019 EBITDA. Like MSELF loans, MSPLF loans have a principal amortization of 15% at the end of the second year, 15% at the end of the third year, and a balloon payment of 70% at the end of the fourth year, according to the term sheet.

Unlike the PPP, loans provided under the MSLP are not eligible for loan forgiveness. Instead, lenders will sell 95% of the MSELF or MSNLF loan, or 85% of the MSPLF loan, to the appropriate special purpose vehicle (SPV) – either the new loan facility or the expanded loan facility. The financial institution would retain 5% or 15% of the loan, respectively, on its books, and the SPV would pay the lender an annual fee of 25 basis points of its participation amount for servicing the loan. Meanwhile, lenders would pay the SPV a facility fee of 100 basis point of the principal amount of the loan participation purchased by the SPV, but the lender may require the borrower to pay this fee, according to term sheets for the program.

Unlike the PPP, loans provided under the MSLP are not eligible for loan forgiveness. Instead, lenders will sell 95% of the MSELF or MSNLF loan, or 85% of the MSPLF loan, to the appropriate special purpose vehicle (SPV) – either the new loan facility or the expanded loan facility. The financial institution would retain 5% or 15% of the loan, respectively, on its books, and the SPV would pay the lender an annual fee of 25 basis points of its participation amount for servicing the loan. Meanwhile, lenders would pay the SPV a facility fee of 100 basis point of the principal amount of the loan participation purchased by the SPV, but the lender may require the borrower to pay this fee, according to term sheets for the program.

It has not been announced when the Main Street Lending Program will launch.

Whereas the PPP loans must be used primarily for payroll, funds provided under the MSLP are not so restrictive, although the borrower must agree to make reasonable efforts to maintain employment levels. The borrower must also attest that the proceeds will not be used to repay other debt of equal or lower priority or to repurchase stock, but these restrictions are not uncommon in normal course lending unless the loan is made with that specific purpose in mind. Furthermore, borrowers must also indicate that they require financing due to the impact the coronavirus pandemic has caused. This flexibility will allow businesses to deploy funds to maintain their business during the crisis. The lender must pledge that it won’t cancel or reduce existing lines of credit to the borrower, while the borrower must agree it won’t try to cancel or reduce outstanding lines of credit with any existing lender.

About the Author

Kylee Wooten

Media Relations Manager

Kylee manages and writes articles, creates digital content, and assists in media relations efforts