This post was updated to reflect new compliance deadlines finalized by the CFPB on May 1, 2026.

Lending & Credit Risk

C&I Loans

Commercial Lending

Construction Lending

CRE Lending

Lending Regulation

Loan Origination System

Member Business Lending

Small Business Lending

CFPB 1071 Compliance: Overview, dates, and details

June 17, 2026

0 min read

New timelines for small business loan data collection and reporting

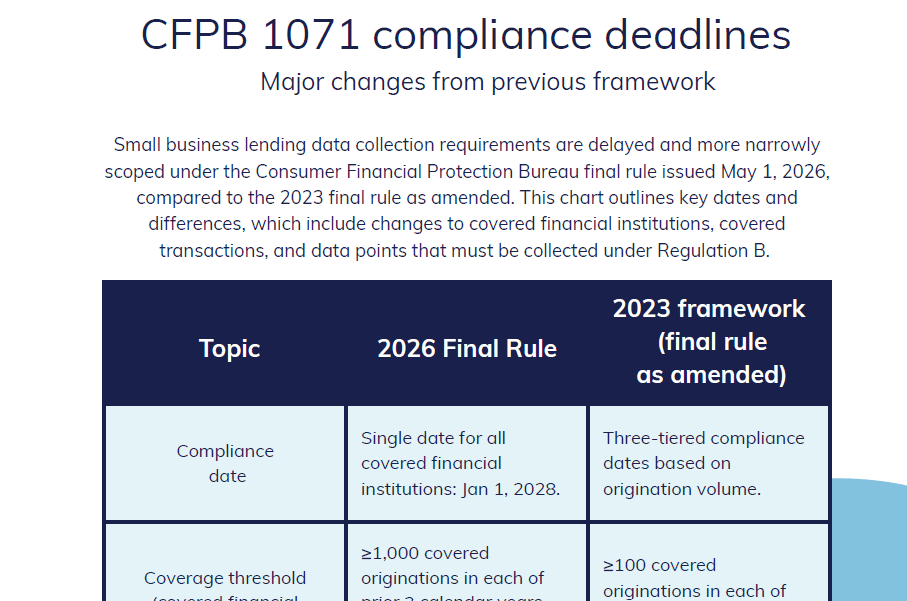

The Consumer Financial Protection Bureau (CFPB) in 2026 issued a final 1071 rule that extends the section 1071 compliance date for all covered financial institutions to Jan. 1, 2028. The new rule for collecting data on small business loan activities replaces a 2023 rule framework and its tiered implementation deadlines.

You might also like this one-page PDF with key dates and details on complying with the 1071 rule.

About the Author

Mary Ellen Biery

Senior Strategist & Content Manager

Mary Ellen Biery is Senior Strategist & Content Manager at Abrigo, where she works with advisors and other experts to develop whitepapers, original research, and other resources that help financial institutions drive growth and manage risk. A former equities reporter for Dow Jones Newswires whose work has been published in