The Issue of Disclosures and the Proposed ASU – Codification Improvements – Financial Instruments

This is the third installment in a series of blog posts about the proposed ASU for codification improvements to ASU 2106-13, better known as the CECL standard.

Issue 5A: Vintage Disclosures – Line-of-Credit Arrangements Converted to Term Loans

One of the new disclosures required by the CECL standard is the disclosure of the carrying value of loans disaggregated on both their credit quality indicator as well as the vintage, or year of origination. The entity would have to produce this disclosure with columns for term loans originated in the last five years, as well as separate columns for term loans originated prior to the last five years and revolving loans. See the below illustrative example directly from the guidance:

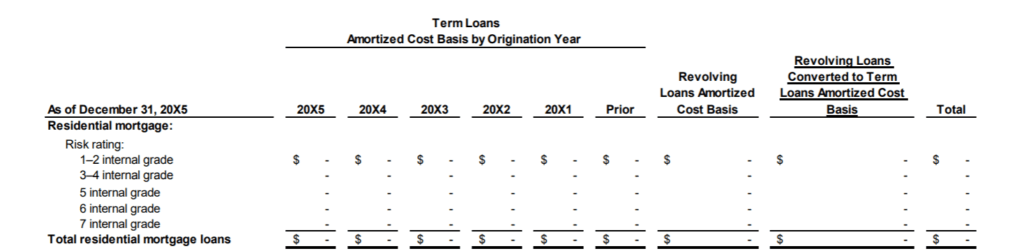

An issue that was discussed at the November 1st meeting of the CECL Transition Resource Group was how loans should be treated in the vintage disclosure that had previously fallen into the revolving category but at some point since have converted to term loans. A variety of scenarios were raised, including revolving loans where an eventual conversion to term was written into the original agreement, or loans where the lender performs a new underwriting and converts the existing revolving loan to a term loan. This also might include loans that are restructured as part of a Troubled Debt Restructure (TDR) agreement. Opinions seemed to differ on what the correct treatment of these loans would be for disclosure purposes: whether they should be included in the column based on their origination date, included in the column the based on the date they converted to term loans, left in the revolving column even after the conversion to term, or allow an entity to make a policy election for which of these approaches to take.

Ultimately, the approach FASB landed on was twofold:

- Any loans that converted to term loans based on a subsequent credit decision would be included in the column that corresponded to the year of that credit decision.

- Any loans that converted from revolving to term without a subsequent credit decision, i.e. those that were written into the original contract of the loan, would be included in a new column on the disclosure specifically for that purpose.

An example of the new disclosure can be seen below:

Abrigo’s Take: In this case, it seems like FASB found a pretty elegant solution to this tricky issue. By basing the inclusion in the term loans column on a subsequent credit decision, this should allow institutions to utilize data fields they are already tracking for other purposes (Last Renewal Date, for example) to also track which vintage year column the loan should appear in for this disclosure. However, institutions may have to look closely at what types of products they have that would fall into the new category outlined here, and make sure that those products are able to be identified for proper placement in this disclosure. Once those product types are identified, it should be simply a matter of combining those product types with whatever revolving indicator is already being used to determine what term loans should fall into this category.