On February 13, the House Financial Services Committee hosted its first hearing on cannabis banking regulation which left a lot of questions still high on bankers’ minds. “Challenges and Solutions: Access to Banking Services for Cannabis-Related Businesses” was intended to start the conversation around federal regulation of banking marijuana-related businesses (MRBs).

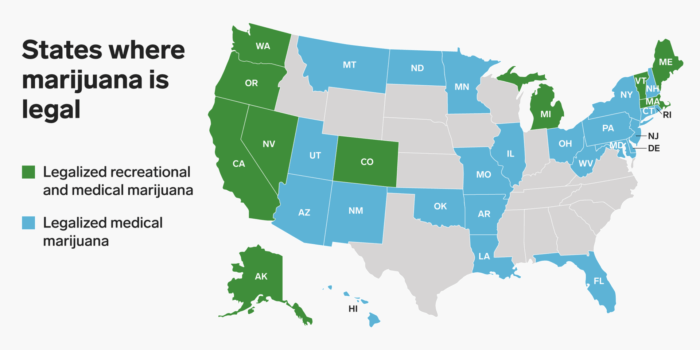

The main issue is that 33 states currently allow legal cannabis use to some extent while it remains completely illegal at the federal level. This means banking MRBs to any extent is still risky and opens a financial institution up to violations of the Bank Secrecy Act (BSA). The main part of this recent hearing focused on Rep. Ed Perlmutter’s (D-CO) draft of the “Secure and Fair Enforcement Banking Act of 2019” (SAFE Banking Act), which drew on the equivalent of the bill introduced in 2017 but added two sections in response to the Department of Justice’s repeal of the Cole Memorandum guidance.

The two additions included:

- “Sec. 3: Treatment of Proceeds Under Federal Law” which addresses the federal criminal money laundering statutes and clarifies that money from a transaction conducted by a legitimate cannabis-related business is not considered proceeds from unlawful activity.

- “Sec. 7: Guidance and Examination Procedures” – requests uniform guidance and exam procedures for financial institutions that provide banking services to MRBs from the Federal Financial Institutions Examination Council (FFIEC).