Dave Koch, Director of Abrigo Advisory Services, also contributed to this article.

Asset/Liability

Asset Liability Modeling

Deposit Modeling

Deposit Pricing Optimization

Portfolio Risk & CECL

Understanding your core deposit study: Reading between the lines

April 28, 2022

0 min read

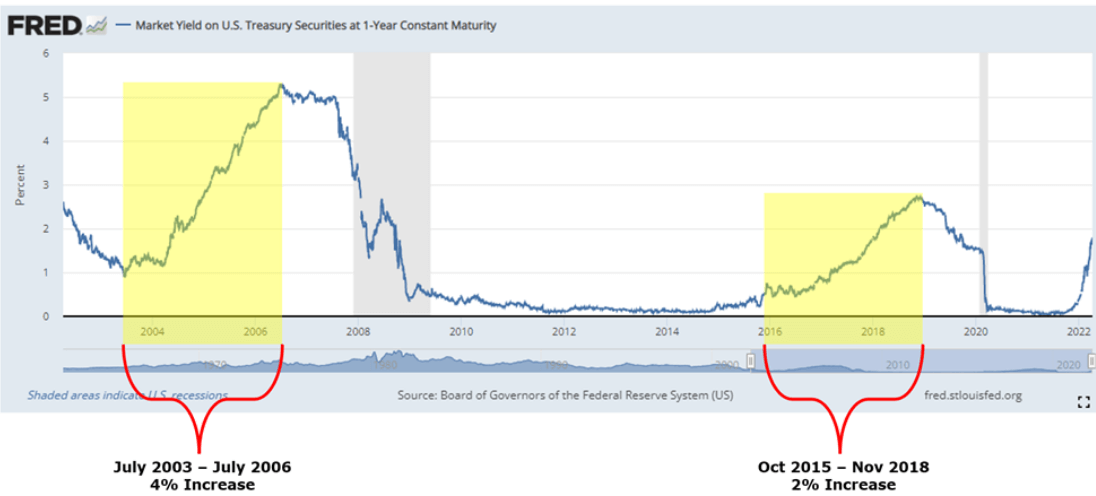

If you look at the last two “up” or rising-rate environments, you might see different pricing strategies used by management to maintain core deposits. For example, coming out of a more volatile rate environment in the early 2000s, customers or members were potentially more rate sensitive. Rates also went up over 4% during that three-year period. That would have driven management teams to use higher betas and shorter lags to keep core deposits. The last rising-rate environment from 2015-2018 was after a prolonged period of almost zero rates. Rates only climbed around 2% over that three-year period. Consumer’s expectations of earning interest were potentially much lower. The steepness of the rate increase was much lower. Management teams might have decided not to pass any rate increases on and were willing to take the risk of losing core deposits. See graph below.

About the Author

Rob Newberry

Senior Consultant

Abrigo

Rob Newberry is Senior Consultant with Abrigo’s Advisory Services and a faculty member of the Graduate School of Banking at the University of Wisconsin-Madison. In the past 10 years, he has worked with financial institution leaders and regulators to develop a suite of credit administration tools for community banks and