Effective loan review has always been critical for managing a financial institution’s credit risk as part of ensuring its safety and soundness. Uncertainty related to the coronavirus pandemic highlighted the importance of identifying loans with actual or potential credit weaknesses as early as possible.

In addition, updated guidance on loan and credit risk review in 2020 emphasized the importance of independent loan review or credit review systems that are tailored to institutions’ specific risks and circumstances.

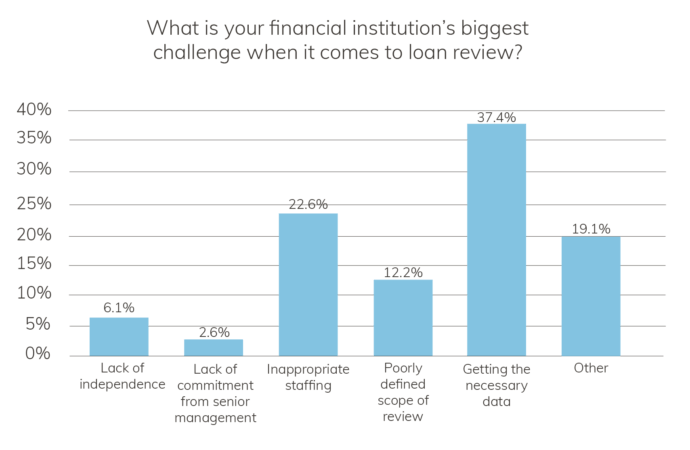

However, loan reviews can only be as accurate as the information used for the review. And as the survey showed, getting the necessary data can be difficult for many financial institutions. Loan reviewers require accurate information at the loan level, which, at many institutions, might be located in multiple systems: