High inflation rates, lingering supply chain issues from the pandemic, and war in Ukraine impacting oil and agricultural commodity prices are all challenges creating a less stable market than in years past. But uncertainty can give financial institutions opportunities to distinguish themselves through commercial loans, which have remained strong through the pandemic. With the right strategies and risk mitigation protocols, banks and credit unions can expand their commercial loan portfolios successfully.

Strategies for growing commercial loans

August 30, 2022

0 min read

There are several benefits to expanding the commercial loan portfolio in today's environment, according to Abrigo Senior Advisor Rob Newberry.

- Typically, financial institutions can get a higher net interest margin opportunity when they book a loan than they can by buying an investment. In a rising-rate environment, it can be difficult to sell and profit from investments that have been locked in for a set term and profit. Rather than buying more investments and incurring unrealized losses, growing the commercial loan portfolio can lead to a greater return on assets (ROA) or return on equity (ROE).

- Collateral-backed real estate loans and high property values make commercial real estate a worthwhile investment in these inflationary times. Commercial real estate (CRE), like other tangible assets, tends to appreciate in value proportionate to inflation, so while it is important to be careful of bubbles in certain markets, these loans could be a great investment.

- The lack of alternative options in a rising-rate environment may be a factor when deciding to expand into commercial lending. With bond markets down and low Treasury yields, there are few other places institutions can put money into and get a return.

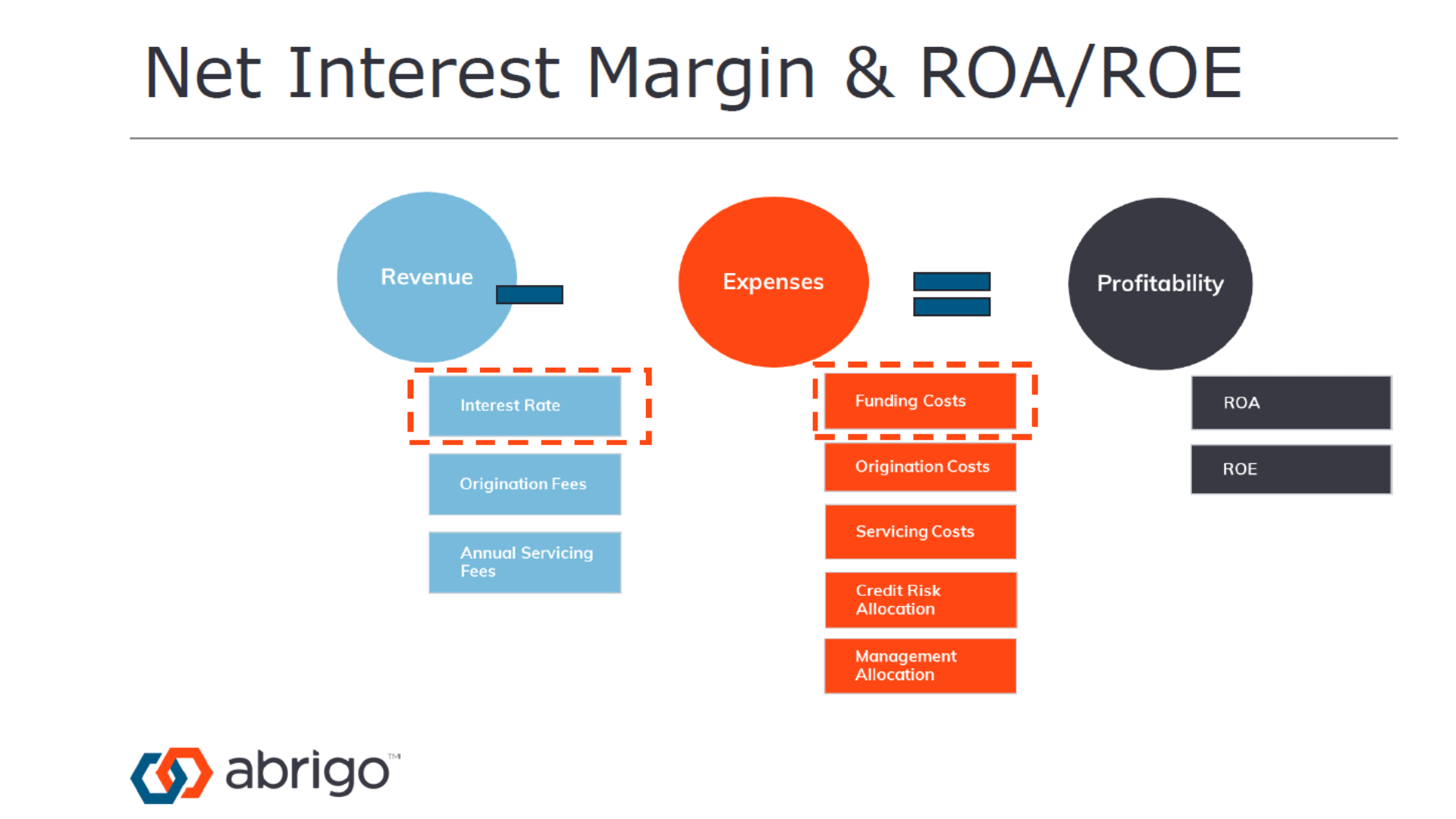

Before increasing commercial loans, think through their profitability and ensure prices set by your institution make sense using the following guide. The net interest margin is a main component of ROA and ROE calculations. Interest rates generate most of the net interest margin, while funding costs, depending on how they are migrated with the increasing fed rates, are the biggest expense. During Abrigo’s Strategies to Growing Your Commercial Loan Portfolio webinar, Newberry posited the following chart to help visualize the calculation:

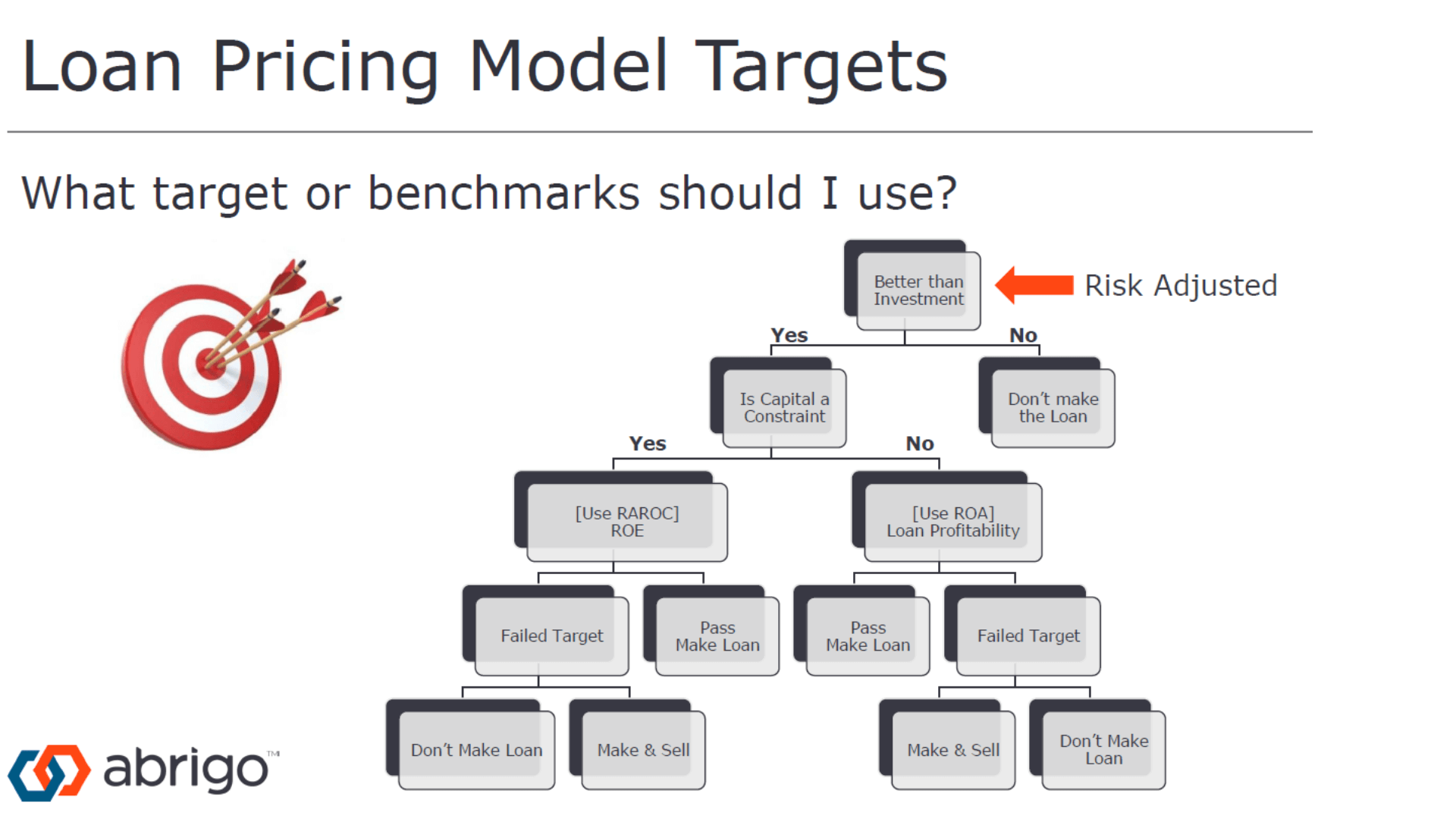

According to Newberry, the first question an institution should ask itself when pricing commercial deals is whether it is a better choice than an investment once credit risk is factored in. With liquidity rates what they are today, that may be an easy “yes.” From there, decide whether to use ROA or ROE to calculate price. Finally, ask if the loan as priced will meet your institution’s target ROA or ROE expectation. If it will be a profitable move, make the loan. Reference the flow chart below to ensure consistency with these decisions.

About the Author

Kate Randazzo

Content Marketing Manager

Abrigo

Kate Randazzo is a Content Marketing Manager at Abrigo, where she works with industry thought leaders to create digital content that helps financial institutions better serve their customers. Before joining Abrigo, Kate managed social media and produced articles for Campbell University’s quarterly magazine and other university content initiatives. She earned