Pervasive inefficiency related to data entry is one of the problems. At most banks and credit unions, staff re-enter the same data point between 1 and 5 times, according to the survey.

Abrigo Credit Consultant John Millman said that when institutions use multiple, unconnected systems, staff must repeatedly enter the same information. That wastes time and risks data entry errors.

About 1 in every 5 bankers at financial institutions with more than $500 million in assets said the same data is entered up to 10 different times. As banks or credit unions grow their assets, it's likely that an increased number of loan applications contributes to the expansion, but repetitive data entry can quickly add up to higher staffing costs that eat into profitability.

“Maybe they kick off the data-entry process by having a lender enter customer info into a [customer relationship manager software], but if that CRM doesn’t integrate into their core, then someone at the institution has to take that info and enter it in the core system,” he said. “If they pull credit for loans, that same customer info has to be put into whatever system they pull credit from. If they need to look up OFAC separately from credit reporting, then they would pull OFAC in another system. Before closing a loan, they need to look up any outstanding UCCs or liens to ensure the institution is in first position, and this is another system or website where they would search. The list goes on, and we haven’t even gotten into creating closing documents or credit presentations. The amount of times in the lending process that the same info needs to be entered could be massive.”

If financial institutions have inefficient processes now, it’s vital that they address them if they are to compete effectively for fewer borrowers and manage any increased credit risks arising if the economy weakens. Many community bankers expect a recession will start by at least mid-2021, according to the most recent Community Bank Sentiment Index.

“I’m surprised at how inefficient and poorly automated things are,” said David O’Connell, Senior Analyst with research firm Aite Group, after reviewing the survey results. Lending, he noted, is the “tip of the spear” – the activity that gets a financial institution into a business, allowing it to deploy its capital and create a profit through lending as well as cross-selling other products or services that can carry high margins, such as treasury management, corporate cards, or wealth management services.

Efficiency in these essential lending and credit operations ensures a good customer experience, instills discipline for underwriting quality control, and helps meet institutional financial goals, according to O’Connell and others.

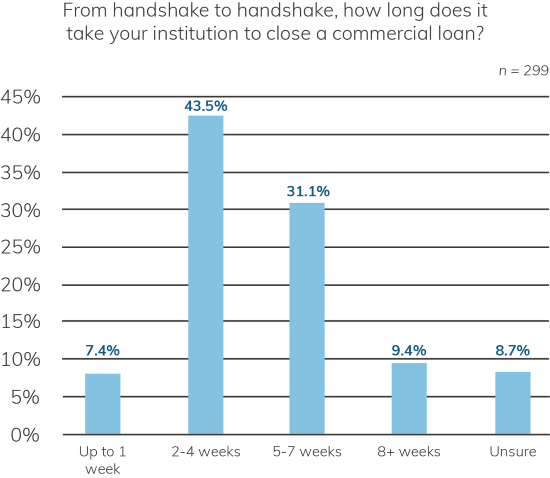

The types of inefficiencies and delays are those that can also result in unhappy customers and staff.

The types of inefficiencies and delays are those that can also result in unhappy customers and staff.