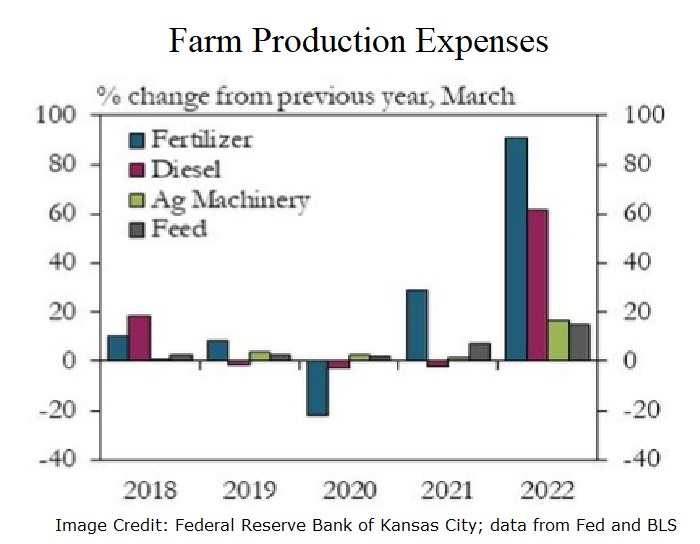

Russia’s invasion and policy responses affecting trade sent global commodity markets into turmoil, given those countries’ production and export of wheat, corn, oil, and natural gas. In addition, the Federal Reserve increased the federal funds rate in May and June, boosting it by 125 basis points and pledging additional hikes if necessary to contain inflation.

With the USDA’s next Farm Sector Income Forecast not published until September, this article examines the February expectations and factors that will likely influence the updated ag sector outlook.

Ag receipts higher on pricing, volume

February’s farm sector forecast said direct government farm payments this year would drop 57% from last year’s levels as the disaster assistance and supplemental help tied to the coronavirus ends. Direct government farm payments, which exclude USDA loans and insurance payments from the Federal Crop Insurance Corp., were more than one-tenth of gross cash farm income in 2020. This year, direct payments were expected to be around 2%, which is closer to the 2015-2018 average of about 3%.

Despite the return to more normal levels of direct government support, farm cash receipts were forecasted in February to be up by nearly 7% to $461.98 billion in nominal dollars. “In 2022, both increasing prices and quantities sold are expected to have positive effects on cash receipts,” the USDA’s Economic Research Service said.

The government expected increased receipts for milk, cattle/calves, and broilers to contribute to nearly 9% growth in animal/animal product receipts (up $17.4 billion to $213.3 billion). It said soybean, corn, cotton, and wheat combined would generate nearly all of the forecasted 5.1% annual growth in crop receipts (increasing by $12 billion to $248.6 billion).

Those forecasts don’t consider the impact of several commodity prices surging to historically high levels after Russia’s invasion. The Kansas City Fed reported in May that wheat and corn prices were 60% and 30% higher, respectively, than a year earlier at the end of the first quarter. Ag prices more broadly had jumped 30% from a year ago and rose 12% from the fourth quarter.