- This Abrigo article was originally published August 7, 2026 on Monitor Daily.

How a financial institution responds to fraud makes a difference

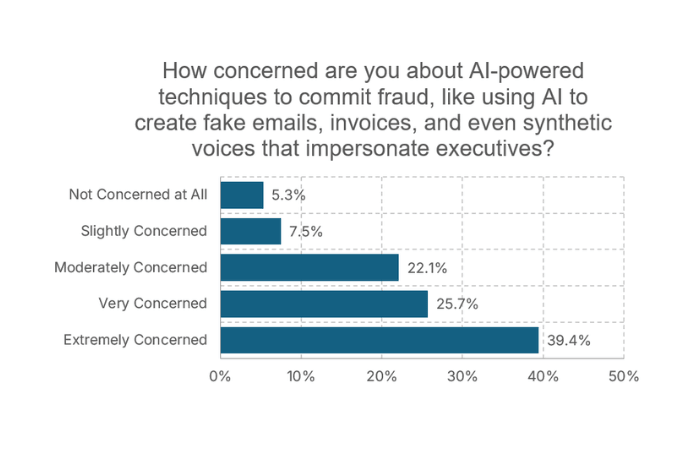

Consumers are decidedly receptive to the concrete results that AI-powered fraud detection enables, according to Abrigo's 2026 State of Fraud Survey.

Key topics covered in this post:

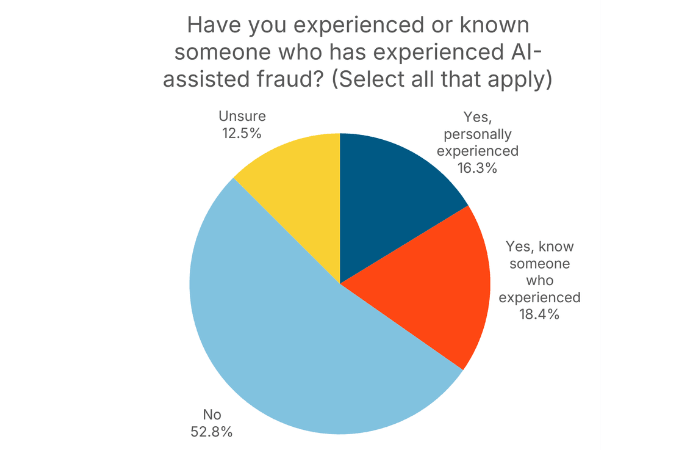

Firsthand experience with AI fraud

Fortunately, concern does not necessarily reflect widespread firsthand experience with AI-assisted fraud.

About 1 in 6 consumers have personally experienced it, while nearly 1 in 5 know someone who has. Consumers ages 25 to 44 were the most likely to have either experienced AI-assisted fraud themselves or know someone who has.

Consumers want confidence in concrete protections

Given their experience and concern, customers want and need confidence that their financial institution can:

- detect fraud danger quickly

- understand a transaction alert

- communicate when needed

- respond quickly to prevent or limit damage.

In fact, 3 out of 5 consumers said being a victim of fraud would make them more likely to minimize their banking relationship with a financial institution.

The good news for financial institutions is that clients do not need to know about every tool in the fraud stack for effective tools to create value. Many consumers do not know whether AI is already part of their institution’s fraud defenses. In Abrigo’s survey, 55.7% of consumers (and 84.4% of consumers 65 and older) do not know whether their current bank or credit union uses AI-enabled fraud-detection tools. Only 18.9% said they do know.

That uncertainty may be tempering enthusiasm for AI tools and may reflect an opportunity for customer or member education. Nearly half of consumers, 45.6%, said they need more information to say whether AI is effective at fraud detection. And when asked if they’d feel more confident in their institution’s ability to detect fraud if it used AI tools, respondents were roughly split among yes, no, and “I don’t know.”

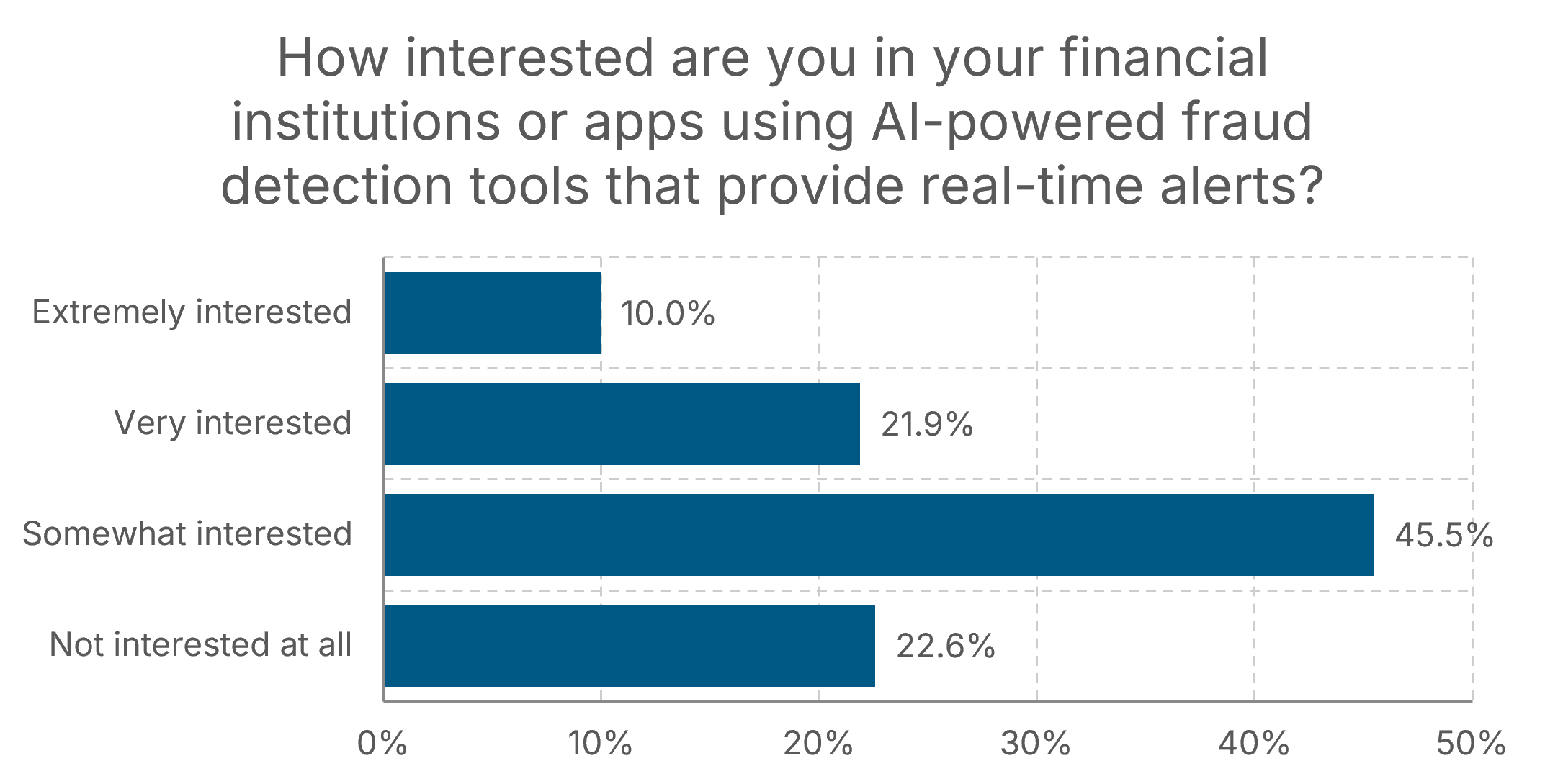

But consumers are decidedly receptive to the concrete results that AI fraud detection can enable. More than three-quarters of respondents, 77.4%, said they were at least somewhat interested in financial institutions or apps using AI detection tools that provide real-time alerts.

When asked what would make them more secure in their banking experience:

- 1% selected faster alerts and automatic transaction blocking.

- 7% selected stronger authentication methods.

- 9% selected AI-driven fraud detection that learns from spending habits.

Managing risk amid economic uncertainty

Even with unclear economic outlooks, financial institutions can make sound risk management decisions. Learn how to get more value from required risk management activities.

Key topics covered in this post:

Risk factor review

The following sections provide additional detail and potential questions to aid in analyzing each risk factor as part of the AML/CFT risk assessment.

Products and services

Products and services

Understanding the financial institution's products and services involves knowing how many customers or members use these services and the risks involved in those products or services. For example, the following questions may be asked:

- Does the FI offer the sale of monetary instruments?

- Are monetary instruments allowed to be sold to non-accountholders?

- Do you allow customers or members to send outgoing international wires?

- If so, how is this monitored?

- How many accounts and to which countries are they sent?

- Do you offer services to those without a Tax ID Number (TIN)?

- If so, how many customers or members?

Although not all-inclusive, other products and services that you may want to include in your review are:

- Foreign correspondent accounts

- Special use accounts

- Trade finance

- Bulk cash

- Consumer or business loan portfolios

- Online account access/opening

- ATM services

- Remote deposit capture

Remember, it’s essential to understand whether these volumes are increasing or decreasing and what controls are in place to mitigate the inherent risk. Once again, all supporting documentation of your analysis must be retained.

Geography

Geography

To analyze geography, understanding the branch footprint of the financial institution is critical. Specific questions to ask include:

- What are the area's populations of cities and towns?

- Are the branches located within High-Intensity Financial Crime Areas or High-Intensity Drug Trafficking Areas?

- Does the financial institution have a presence on the U.S.-Mexico border?

- Does the institution file many suspicious activity reports (SARs) annually compared to the other institutions in the same geographical area? If not, what might be the reason?

Determine whether these volumes are increasing or decreasing and what controls the bank or credit union has for each customer or Member Base.

The customer or member base should be evaluated on several factors, such as the number of high-risk customers or members of the financial institution. Consider the following types of customers in your account base:

- Non-Resident Aliens (NRAs)

- Politically exposed persons (PEPs)

- Cash-intensive businesses (including marijuana-related businesses)

- Money Services Businesses (MSBs)

- Virtual currency exchanges

- Non-bank financial institutions (NBFIs)

- Professional service providers

In addition, the risk assessment will want to include assessing how well the financial institution collects beneficial ownership information and whether the customer due diligence (CDD) and enhanced due diligence (EDD) processes are sufficient. Again, determine if these volumes are increasing or decreasing and what controls are in place. These questions must be answered to understand the customer or member risk fully.

Transactions

Transactions

Transactions will require a review of both volumes and frequencies. Analyze processes such as:

- Number of currency transaction reports (CTRs) filed annually

- Number of SARs filled annually

- Volumes and frequencies of international wires compared to domestic

- Number of international ACH transactions compared to domestic transactions

- The volume of Private ATM customers, if any

- The volume of loan transactions

FinCEN Priorities

FinCEN Priorities

FinCEN issued eight National AML/CFT priorities in June 2021. Each of the following priorities should have a section within the risk assessment addressing the institution’s risk and any mitigating factors available for each risk:

- Corruption

- Cybercrime and related cybersecurity, including virtual currency considerations

- Foreign and domestic terrorist financing

- Fraud

- Transnational criminal organizations (TCO) activity

- Drug trafficking organizations (DTO) activity

- Human trafficking and human smuggling

- Proliferation financing (weapons and materials of mass destruction)

Staffing

Staffing

Adequate compliance staffing is critical to any AML program. When analyzing human resources for your risk assessment, consider the following:

- Number of full-time and part-time employees in AML function

- How these numbers compare to the previous year

- Qualifications and experience level of the AML staff

- What training is provided for the team (and the financial institution staff more broadly)

- Whether background checks are conducted when hiring

Regulatory audit and exams

Regulatory audit and exams

Regulatory audit and exam results demonstrate a picture of your AML program's health and any gaps that may be present in the program. If the institution has a history of violations, particularly repeat findings, the risk of the financial institution should be increased in the risk assessment. Suppose the board of directors has been adequately apprised of the audit or exam outcomes, and repeat violations occur. In that case, this could indicate a need for a strong culture of compliance, which will ultimately lead to further increased risk. The following other items should also be addressed within an audit or exam:

- Policies and procedures should be checked and updated when necessary.

- A designated officer should be appointed and approved by the board of directors as responsible for AML/CFT and OFAC compliance.

- SARs and CTRs should be filed regularly and promptly, following FinCEN guidelines.

OFAC

OFAC

Adequate OFAC compliance is essential for mitigating a financial institution’s risk. A robust OFAC risk assessment supporting the program is critical to avoid costly monetary penalties or regulatory consent orders. Certain transactions, such as wire transfers and ACH, must be checked for OFAC matches before being sent. A financial institution should have a clear set of policies and procedures for OFAC compliance and provide training to all stakeholders. If the institution has a history of OFAC violations, the OFAC risk should be classified as elevated and tightened with mitigating factors.

Trusting the numbers too much

Trusting the numbers too much

Financial statements remain the foundation of commercial credit analysis, but reported earnings, strong leverage ratios, or favorable debt service coverage can create confidence that isn't always warranted.

Profitability does not necessarily translate into cash generation, and borrowers with healthy-looking financial statements may still experience significant liquidity pressure. Working capital trends, changes in receivables, inventory turnover, or payment behavior often reveal developing stress well before earnings begin to decline.

Likewise, management adjustments, normalization assumptions, and optimistic projections deserve thoughtful scrutiny rather than automatic acceptance.

You might also like this webinar, "Borrower assessment mistakes: Looking beyond the financial statements"

Watch the webinar Failing to understand the business

Failing to understand the business

Hand in hand with not relying solely on numbers is a second mistake: failing to understand the nature of a borrower's business. During the webinar, Kirby encouraged lenders to replace technical interrogation with genuine curiosity.

Rather than asking a borrower to explain maintenance capital expenditures, ask, "What did you have to replace last year?" Instead of questioning a growth projection, ask, "What are you planning to do to grow the business?" Those conversations often reveal risks or strengths that financial statements alone cannot. As Kirby noted, most business owners enjoy talking about their businesses. If they don't, that itself may be a warning sign.

A working capital line, an equipment loan, and a growth investment each carry different risks and require different analytical approaches. Looking at every loan through the same financial lens can cause lenders to focus on the wrong issues and miss what really drives repayment.

To sum up these first two common errors: "Don't mistake precision for understanding the business," Kirby said. “A lender focused only on declining ratios might downgrade the loan unnecessarily. A lender who understands the borrower's plan sees temporary weakness as part of a long-term strategy.”

Missing early signs of deterioration

Missing early signs of deterioration

Problem loans rarely become problems overnight. Most begin with relatively small warning signs that are easy to explain away: slowing receivable collections, inventory growth, repeated covenant exceptions, declining margins, or subtle shifts in management behavior.

One common challenge is delayed risk recognition. Over time, covenant exceptions may become routine, annual reviews can turn into documentation exercises, and lenders may become accustomed to explaining away incremental deterioration rather than investigating its cause.

Strong portfolio monitoring means revisiting the original underwriting assumptions throughout the life of the loan. Are the conditions that supported the original approval still valid? Has the borrower's business changed? Have industry conditions shifted? Are management's original projections still realistic?

Kirby emphasized that rapid growth can consume cash just as quickly as declining performance. Lenders should investigate why cash is disappearing before assuming deterioration.

Every review should ask whether the borrower's story has changed and whether previously identified risks are evolving. Recognizing early warning signs allows financial institutions to engage borrowers sooner, explore potential solutions, and reduce the likelihood that manageable issues become significant credit problems.

Letting bias shape credit decisions

Letting bias shape credit decisions

Even experienced lenders are susceptible to biases that influence judgment. Confirmation bias encourages analysts to seek information that supports their existing conclusions while overlooking contradictory evidence. Strong customer relationships may create pressure to maintain favorable opinions despite emerging concerns. Groupthink can discourage individuals from asking difficult questions during committee discussions, while overconfidence may lead experienced lenders to underestimate evolving risks.

These influences often feel reasonable in the moment because they reinforce existing beliefs. Unfortunately, assumption-driven decisions can quickly unravel when business conditions change.

Healthy credit cultures recognize that thoughtful disagreement strengthens decision-making. Institutions that encourage independent thinking, constructive debate, and objective review are often better positioned to identify mistakes in credit analysis before they affect portfolio performance.

Kirby admitted that early in his career, he had a tendency to pay less attention to guarantors and care mostly about cash flow. Later, he realized that guarantors can either strengthen or weaken a deal depending on their own financial position. His lesson: Every experienced lender develops biases. Good credit culture requires recognizing those biases before they shape lending decisions.